Working as a 1099 contractor has become increasingly popular in today’s gig economy, offering flexibility and independence that traditional employment simply cannot match. However, this employment classification comes with significant tax implications, financial responsibilities, and administrative requirements that many freelancers underestimate. Understanding what a 1099 job truly entails—from tax obligations to quarterly payments—is essential before making the leap from W-2 employment to independent contracting.

The IRS Form 1099 represents a fundamental shift in how you’ll manage your career, finances, and business operations. Unlike traditional employees who receive W-2 forms with taxes already withheld, 1099 contractors must navigate self-employment taxes, quarterly estimated payments, deductible business expenses, and comprehensive record-keeping. This guide combines expert tax insights with practical career advice to help you understand whether 1099 work aligns with your professional goals and financial situation.

What Is a 1099 Job: Definition and Basics

A 1099 job refers to independent contractor work where compensation is reported on IRS Form 1099-NEC (for nonemployee compensation) or Form 1099-MISC. This employment classification means you are self-employed, working for yourself rather than as an employee of a company. The IRS considers you a business owner responsible for managing your own taxes, benefits, and business operations.

When you accept a 1099 position, you’re entering into a contractual relationship where the hiring company pays you for specific services or deliverables without providing employee benefits, tax withholding, or employer-sponsored insurance. This arrangement offers remarkable flexibility—you can often work on your own schedule, choose multiple clients, and build a diverse income portfolio. However, this freedom comes with substantial financial and administrative responsibilities that require careful planning and execution.

The key distinction lies in control and independence. The IRS determines contractor status based on factors like whether the company controls how you work, whether the relationship is permanent or project-based, and whether you provide your own tools and workspace. Understanding these nuances helps you recognize legitimate 1099 opportunities and avoid misclassification situations.

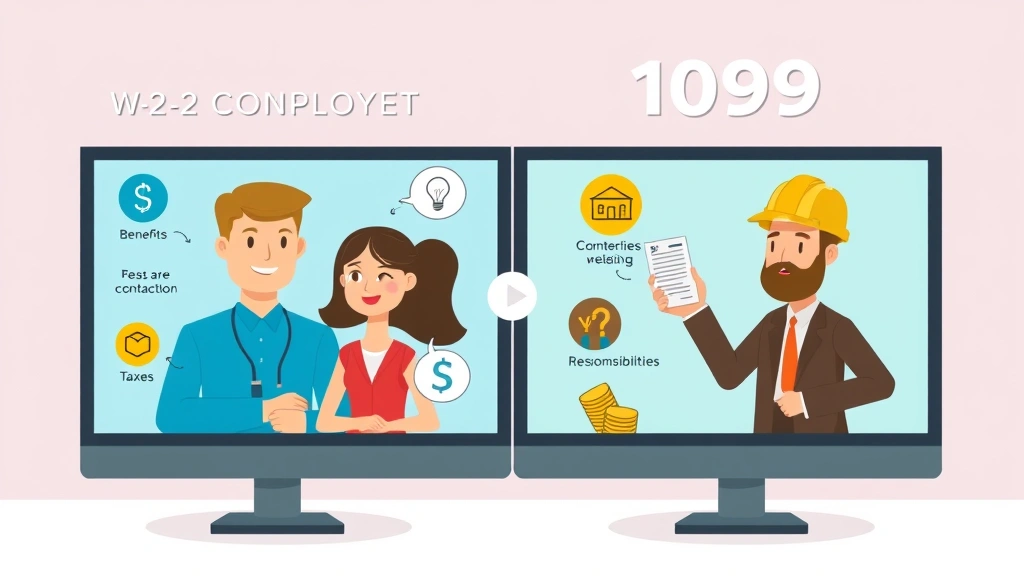

1099 vs W-2 Employment: Key Differences

The differences between 1099 contractor work and traditional W-2 employment extend far beyond tax forms. Understanding these distinctions is crucial for making informed career decisions and properly managing your finances.

Employment Classification and Control: W-2 employees work under employer supervision with the company controlling how, when, and where work is performed. 1099 contractors maintain independence, determining their own work methods and schedules. This fundamental difference affects everything from scheduling flexibility to liability responsibility.

Tax Withholding and Responsibility: Employers automatically withhold federal income tax, Social Security, and Medicare taxes from W-2 paychecks. With 1099 work, you receive full payment and must calculate and pay all taxes yourself. This requires understanding quarterly estimated payments and self-employment tax calculations.

Benefits and Insurance: W-2 employees typically receive health insurance, retirement plan contributions, paid time off, and workers’ compensation coverage. 1099 contractors must independently obtain and pay for health insurance, retirement accounts, disability insurance, and any other coverage they want. These costs can significantly impact your net income.

Expense Deductions: While W-2 employees can claim limited itemized deductions, 1099 contractors can deduct legitimate business expenses, reducing taxable income. This includes home office space, equipment, software subscriptions, professional development, and client acquisition costs. Proper expense tracking can substantially lower your tax burden.

Income Stability: W-2 employment typically provides consistent paychecks and job security. 1099 work involves variable income, project-based compensation, and the responsibility of finding and securing your own clients. You must develop business development skills and maintain a pipeline of potential work.

For those interested in creative writing positions, many are structured as 1099 arrangements, offering flexibility for writers managing multiple projects and clients simultaneously.

Understanding Self-Employment Taxes

Self-employment taxes represent one of the most misunderstood aspects of 1099 work. These taxes fund Social Security and Medicare benefits and are calculated separately from federal income tax. As a 1099 contractor, you’re responsible for paying both the employer and employee portions of these taxes—totaling approximately 15.3% of your net self-employment income.

Self-Employment Tax Calculation: The calculation begins with your net profit (gross income minus legitimate business expenses). You multiply this by 92.35% to account for the employer deduction, then apply the 15.3% self-employment tax rate. For example, if you earn $50,000 in gross revenue and have $10,000 in deductible expenses, your net income is $40,000. Multiply by 92.35% to get $36,940, then multiply by 15.3% for self-employment tax of approximately $5,652.

Federal Income Tax: Beyond self-employment taxes, you must also pay federal income tax on your earnings. Your tax bracket depends on your total income and filing status. Many new contractors underestimate this obligation, leading to significant tax bills at year-end.

State and Local Taxes: Depending on your location and client locations, you may owe state income taxes and local business taxes. Some states have no income tax, while others impose substantial rates. Research your specific jurisdiction’s requirements.

The Quarterly Payment Imperative: The IRS requires estimated tax payments quarterly. Failing to make these payments can result in penalties and interest charges, even if you ultimately owe taxes. Planning for these payments prevents financial surprises and penalties.

Quarterly Estimated Tax Payments Explained

Quarterly estimated tax payments are mandatory for most 1099 contractors earning over $400 annually. These payments are due on specific dates: April 15, June 15, September 15, and January 15 (for the previous year). Missing these deadlines triggers penalties that compound your tax liability.

Calculating Quarterly Payments: To estimate quarterly taxes, project your annual income and multiply by your expected tax rate. Divide by four for quarterly amounts. For instance, if you expect $60,000 income with a combined 25% tax rate (self-employment plus federal), your quarterly payment would be approximately $3,750. This is a rough estimate; actual amounts depend on your specific circumstances.

Safe Harbor Rules: The IRS provides safe harbor protection if you pay 90% of your current year tax liability or 100% of your previous year’s tax liability (110% if your adjusted gross income exceeded $150,000 in the prior year). Many contractors use the previous year method for simplicity, though this may result in underpayment if income increases significantly.

Payment Methods: The IRS accepts estimated tax payments through their website (IRS.gov), by phone, or by mail using Form 1040-ES. Setting up automatic payments eliminates the risk of missed deadlines and ensures consistent tax management.

Adjusting Payments Throughout the Year: If your income fluctuates significantly, recalculate quarterly payments accordingly. Overpaying early in the year and underpaying later can result in penalties. Conversely, accurate quarterly payments prevent year-end surprises and penalties.

Deductible Business Expenses for Contractors

One significant advantage of 1099 work is the ability to deduct legitimate business expenses, directly reducing your taxable income. Understanding which expenses qualify is essential for maximizing tax efficiency and maintaining IRS compliance.

Home Office Deduction: If you maintain a dedicated workspace exclusively for business, you can deduct a portion of rent, utilities, insurance, and maintenance. The simplified method allows $5 per square foot (maximum 300 square feet), totaling up to $1,500 annually. The detailed method requires calculating actual expenses proportional to office space.

Equipment and Technology: Computers, software subscriptions, phones, internet service, and professional tools are deductible if used primarily for business. Office furniture, filing systems, and workspace organization expenses also qualify. Depreciation rules may apply to expensive equipment.

Professional Services and Fees: Accounting, legal consultation, bookkeeping software, tax preparation, and business coaching expenses are fully deductible. These services help you manage your business more effectively and ensure tax compliance.

Transportation and Travel: Mileage for client meetings, project research, or business development is deductible at the IRS standard mileage rate (updated annually). Airfare, hotels, and meals for business travel are deductible, though meal expenses are limited to 50% of actual costs.

Professional Development: Courses, certifications, conferences, and training related to your business are deductible. Industry publications, memberships, and continuing education maintain your professional competitiveness and are tax-deductible.

Marketing and Advertising: Website hosting, domain registration, business cards, advertising, and client acquisition costs are deductible business expenses. Social media marketing tools and professional photography for your online presence qualify.

Insurance Premiums: Health insurance premiums for self-employed individuals are deductible. Professional liability insurance, general business insurance, and disability insurance are also deductible.

Record-Keeping and Documentation Requirements

The IRS requires 1099 contractors to maintain meticulous records supporting all income and expense claims. Proper documentation protects you during audits and ensures accurate tax reporting.

Income Documentation: Keep all 1099 forms received from clients, along with invoices, payment receipts, and bank statements showing deposits. Maintain records of contracts and agreements detailing payment terms and project scope. Digital or physical copies of these documents should be organized and easily retrievable.

Expense Records: Maintain receipts for all business expenses, including digital receipts from online purchases. Credit card and bank statements provide backup documentation. For mileage, keep a log with dates, destinations, mileage, and business purpose. Photography of receipts helps create backup records.

Accounting Systems: Use accounting software like QuickBooks, FreshBooks, or Wave to track income and expenses systematically. These platforms generate reports facilitating tax preparation and provide audit trails demonstrating organized record-keeping. Regular reconciliation ensures accuracy.

Retention Requirements: The IRS typically examines returns within three years of filing, though this period can extend to six years for significant underreporting. Maintain records for at least seven years to protect yourself. Some permanent business records should be retained indefinitely.

Tax Professional Collaboration: Work with a CPA or tax professional familiar with self-employed individuals. They can guide record-keeping practices, identify deductible expenses you might overlook, and ensure proper tax reporting. This investment often pays for itself through tax savings.

Finding and Landing 1099 Positions

Securing 1099 work requires different strategies than traditional job hunting. Success depends on understanding where these opportunities exist and how to position yourself effectively.

Freelance Platforms: Websites like Upwork, Fiverr, Toptal, and Guru connect contractors with clients seeking specific skills. Building a strong profile with samples, testimonials, and clear descriptions of your services attracts quality clients. Starting with competitive rates helps build reputation and testimonials.

Professional Networks: LinkedIn is invaluable for 1099 work. Optimize your profile highlighting contractor availability, expertise, and services. Connect with former colleagues, clients, and industry professionals. Many 1099 opportunities come through professional referrals and networking relationships.

Industry-Specific Job Boards: Many industries have specialized job boards featuring 1099 positions. Creative professionals find opportunities on specialized creative platforms. Developers discover tech contract work on dev-focused boards. Research your industry’s primary job boards.

Direct Client Outreach: Identify companies needing your services and contact them directly. Many organizations prefer contractor relationships for specific projects. Personalized outreach demonstrating your understanding of their needs often yields better results than generic applications.

Building Your Professional Brand: A professional website showcasing your portfolio, case studies, and client testimonials establishes credibility. Publishing articles, speaking at industry events, and maintaining an active social media presence positions you as an expert in your field, attracting inbound opportunities.

Those interested in high-paying opportunities without formal degrees often find 1099 positions particularly accessible, as these roles emphasize demonstrated skills over credentials.

Leveraging Your Professional Summary: A well-crafted professional resume summary adapted for contractor platforms clearly communicates your value proposition. Highlight specific expertise, proven results, and the problems you solve for clients.

Setting Your Contractor Rate and Pricing

Determining appropriate rates is one of the most critical decisions for 1099 contractors. Underpricing leaves money on the table and undervalues your expertise, while overpricing may limit client acquisition.

Market Research: Research industry standard rates for your specific skills and experience level. Platforms like Glassdoor, Salary.com, and industry surveys provide rate benchmarks. Geographic location significantly impacts rates—contractors in major metropolitan areas typically charge more than those in smaller markets.

Experience and Expertise Premium: Specialized expertise commands higher rates than general skills. Certifications, advanced degrees, and years of experience justify premium pricing. Building a strong portfolio and client testimonials supports rate increases over time.

Accounting for Business Costs: Your rate must cover self-employment taxes (15.3%), income taxes (estimated 20-35% depending on income and location), health insurance, retirement contributions, equipment, software, and professional development. A common approach is to calculate your desired annual income, add 40-50% for taxes and business costs, then divide by billable hours.

Pricing Models: Hourly rates work well for time-based projects with variable scope. Project-based pricing suits well-defined deliverables and builds client relationships by aligning incentives. Retainer arrangements with regular monthly payments provide income stability.

Value-Based Pricing: For experienced contractors, value-based pricing ties compensation to results or client value received rather than time invested. This approach rewards efficiency and expertise but requires strong client relationships and clear outcome metrics.

Rate Adjustments: Increase rates annually as your experience grows and demand increases. Existing clients may resist increases, but new clients typically accept current market rates. Phased increases maintain client relationships while improving profitability.

Common 1099 Job Categories

1099 work spans virtually every industry and skill level. Understanding popular categories helps identify opportunities matching your expertise.

Creative and Writing Services: Graphic designers, copywriters, content creators, and video producers frequently work as 1099 contractors. Creative writing positions particularly align with contractor arrangements, allowing writers to manage multiple clients and projects simultaneously.

Technology and Development: Software developers, web designers, data analysts, and IT consultants are in high demand as contractors. Software testing positions frequently operate under 1099 arrangements, with testing performed remotely on project basis.

Marketing and Business Services: Digital marketers, social media managers, SEO specialists, and business consultants work extensively as 1099 contractors. These roles leverage specialized expertise for multiple clients simultaneously.

Professional Services: Accountants, lawyers, HR consultants, and business coaches frequently operate as independent contractors. Professional expertise commands premium rates and attracts long-term client relationships.

Customer Service and Support: Technical support specialists, customer service representatives, and virtual assistants work as 1099 contractors for companies seeking flexible, scalable support. Remote work arrangements make these roles accessible to distributed workforces.

Administrative and Back-Office Work: Bookkeeping, data entry, administrative assistance, and project coordination are frequently outsourced to 1099 contractors. These roles often feature flexible hours and remote work options.

Specific 1099 job listings and additional opportunities showcase the diversity of available positions across industries and experience levels.

Legal and Compliance Considerations

Operating as a 1099 contractor involves legal obligations beyond tax considerations. Understanding these requirements protects your business and ensures compliance.

Contractor vs. Employee Misclassification: The IRS has specific criteria for determining whether a worker should be classified as an employee or contractor. Factors include the level of control exercised, investment in business, permanence of relationship, and whether work is integral to the business. Misclassification can result in substantial penalties for both contractor and employer. If you believe you’re misclassified, consult a legal professional or contact the Department of Labor.

Business Structure and Licensing: Consider whether to operate as a sole proprietor, LLC, S-Corp, or C-Corp. Each structure offers different tax advantages, liability protection, and administrative requirements. Consult a business attorney or accountant to determine the optimal structure for your situation. Some jurisdictions require business licenses or permits for specific contractor work.

Contracts and Agreements: Always execute written contracts with clients detailing scope of work, payment terms, deliverables, timelines, and intellectual property ownership. Clear contracts prevent disputes and provide legal protection. Consider having an attorney review standard contract templates before using them repeatedly.

Insurance and Liability: Professional liability insurance protects you if client work causes financial damage. General business insurance covers property and liability. Some industries require specific insurance types. Review insurance needs with a business insurance broker.

Tax Compliance and Penalties: Failure to file required tax forms, make quarterly payments, or report all income triggers IRS penalties and interest. The IRS actively pursues contractor tax compliance. Maintaining accurate records and meeting all deadlines prevents costly penalties.

State and Local Requirements: State and local jurisdictions may impose business registration, licensing, or tax requirements. Research your specific location’s requirements. Some states require contractor registration, while others impose gross receipts taxes or other business taxes on contractor income.

Professional Liability and Malpractice: Depending on your field, professional liability insurance or malpractice insurance may be essential. These policies protect against claims that your work caused financial damage or professional harm to clients.

” alt=”Cartoon illustration of a professional contractor managing multiple projects on laptop, with calendar, invoices, and tax forms organized on desk” style=”max-width: 100%; height: auto;”>

Frequently Asked Questions

What is the main difference between a 1099 contractor and a W-2 employee?

The primary difference is that 1099 contractors are self-employed and responsible for calculating, filing, and paying all their taxes, including self-employment taxes. W-2 employees have taxes withheld by their employer. 1099 contractors also don’t receive employee benefits like health insurance, retirement contributions, or paid time off. Contractors maintain independence in how they work, while employees work under employer supervision.

How much should I set aside for taxes as a 1099 contractor?

A practical rule of thumb is to set aside 25-40% of gross income for taxes, depending on your tax bracket, location, and deductible expenses. This covers self-employment taxes (15.3%), federal income tax (10-22% depending on bracket), and state/local taxes (varies by location). Working with a tax professional helps calculate accurate amounts based on your specific situation. Many contractors open separate savings accounts specifically for quarterly tax payments.

Can I deduct home office expenses as a 1099 contractor?

Yes, if you maintain a dedicated workspace exclusively for business. The simplified method allows $5 per square foot (maximum 300 square feet) for up to $1,500 annually. The detailed method requires calculating actual expenses proportional to your office space relative to total home square footage. Documentation of your office setup and exclusive business use is required for IRS compliance.

What happens if I don’t make quarterly estimated tax payments?

The IRS charges penalties and interest on underpaid quarterly taxes. Safe harbor rules protect you if you pay 90% of current year taxes or 100% of prior year taxes (110% if prior AGI exceeded $150,000). Missing payments can result in substantial penalties, especially if you owe significant taxes at year-end. It’s better to overpay slightly than underpay and face penalties.

Do I need to register my 1099 business formally?

Requirements vary by location and business structure. Many jurisdictions require business registration or licensing. Consider whether to operate as a sole proprietor, LLC, S-Corp, or C-Corp—each offers different tax advantages and liability protection. Consult a business attorney or accountant in your jurisdiction to determine specific requirements and the optimal structure for your situation.

How do I find legitimate 1099 job opportunities?

Legitimate opportunities exist on freelance platforms (Upwork, Fiverr, Toptal), industry-specific job boards, LinkedIn networking, and direct client outreach. Build a strong professional brand through a portfolio website and active industry presence. Beware of opportunities requiring upfront fees or guaranteeing unrealistic income. Established platforms with review systems and payment protection offer safer environments for new contractors.

What records should I keep as a 1099 contractor?

Maintain copies of all 1099 forms, invoices, payment receipts, contracts, bank statements, and business expense receipts. Keep mileage logs for travel deductions. Organize records by category (income, expenses, equipment, etc.) for easy reference. Retain records for at least seven years to protect against IRS audits. Digital storage with backup copies provides security and accessibility.

Can I switch between 1099 and W-2 work?

Yes, many professionals maintain both 1099 contractor work and W-2 employment simultaneously. Combine them strategically—perhaps full-time W-2 employment with supplemental 1099 work. However, ensure your W-2 employer permits outside contractor work, as some employment agreements restrict outside activities. Tax implications of combined income require careful planning and professional guidance.

Authoritative Resources for 1099 Contractors

- IRS Self-Employed Individuals Tax Center – Official IRS guidance on self-employment taxes, estimated payments, and contractor requirements

- Small Business Administration Financial Management Guide – Comprehensive resource for business accounting, tax planning, and contractor financial management

- Society for Human Resource Management – Contractor Classification – Expert insights on proper contractor classification and compliance from leading HR professionals

- Freelancers Union – Advocacy organization providing resources, guides, and community support for independent contractors and freelancers

- QuickBooks Self-Employed Tax Center – Practical tax guidance and tools specifically designed for self-employed individuals and contractors

Final Thoughts: 1099 contractor work offers remarkable flexibility and income potential, but success requires understanding tax obligations, maintaining meticulous records, and developing strong business management skills. The transition from W-2 employment to contractor work represents a significant change in how you approach your career and finances. By educating yourself on tax requirements, maintaining proper documentation, setting appropriate rates, and working with qualified professionals, you can build a sustainable and profitable contractor business. The key is recognizing that operating as a 1099 contractor means operating as a business owner—with all the responsibilities and opportunities that entails.